March 2026: Stocks Down, Bonds Down.

“Bonds aren’t so safe - so welcome to the party!”

However, I’m no Hollywood icon - so I’ll let Bruce have the honors...

Die Hard.

60% stocks for growth, 40% bonds for income and safety. For nearly 40 years, when stocks went down, bonds went up. Said another way, 40 years of declining rates bailed you out.

That inverse relationship ended abruptly in 2022 when the Fed raised rates from near zero to 5%. Bond investors endured a terrible outcome and discovered what duration exposure means….2-3% yields and a huge draw-down of 10-20% or more. In 2022, stocks down, bonds down was a wakeup call – traditional 60/40 was over.

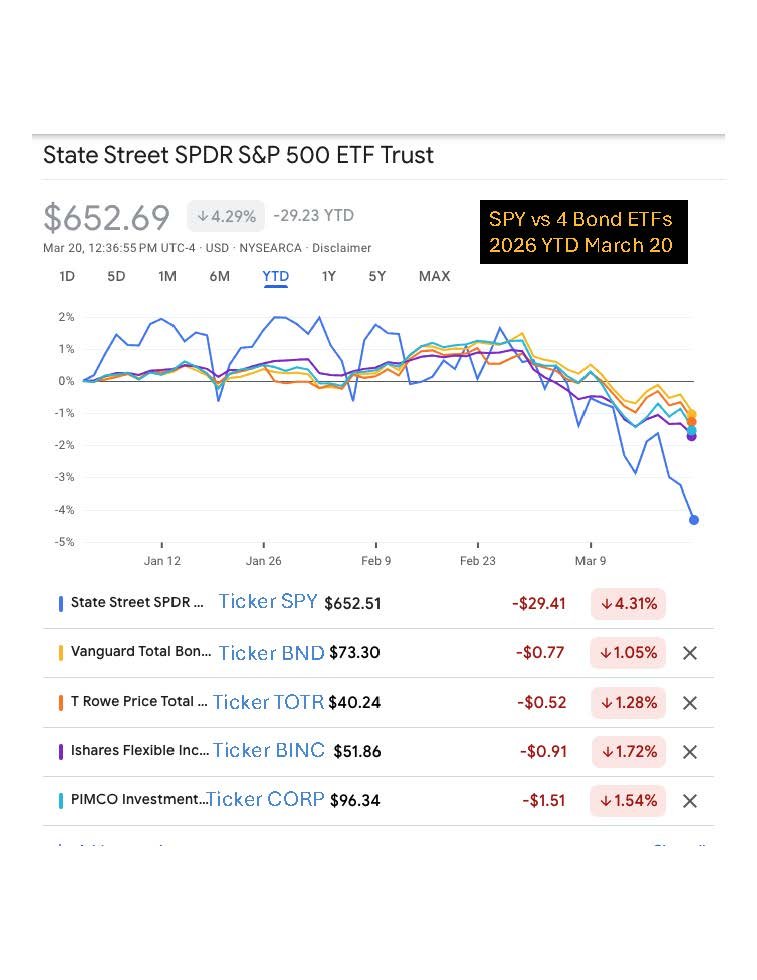

Here we go again…2026 year-to-date: stocks down, bonds down.

US Equities (the S&P 500 for reference) are currently down about 5% YTD after a strong 2025. There are multiple reasons for stocks to endure a pullback in 2026 relative to the “risk on” enthusiasm of 2025.

Bonds down too?…Yep. For 2026 there has been no flight to safety in bonds. Bonds are not offsetting the biggest geopolitical risk event to unfold in a very long time. Traditional bond funds, those with 7 – 10 year duration or longer, are low return at best, their defensive ability has been reduced and there’s good reason to understand why:

Lower interest rates will just boost inflation further. Given the macro environment of mixed economic data, war in Iran, commodity spikes everywhere, pro-growth stimulative policies (govt spending) and other examples – it’s is all inflationary.

Rates are currently not high, FFR is 3.5%. Rates were cut in 2024 and 2025.

Too much debt – There isn’t a lot of demand for US Treasuries at lower rates – the US is expanding its deficits too much, too fast. The market is worried about the US Government’s debt maturity wave and continued spending problems. This keeps rates elevated.

The economy is not weak – if rates are lowered anyway (Trump says we must), surging inflation would be a reckoning for the bond market (rates blow out).

The risk / reward just isn’t there – traditional bond funds are cooked (bonds with intermediate duration of ~7 years or longer).

Own bonds – hold the duration. WLA portfolios are using short-term money market funds as “my favorite bond fund” and maintaining a laddered US Treasury bond portfolio of 1, 2, 3, and sometimes 5 year maturities. Holding to maturity is the goal, accept the income for what it is and manage risk elsewhere.

Look for attractive fixed income alternatives. There are many ways to gain exposure to income paying investments as an alternative to bonds. Dividend focused Equity, Various Energy exposures, REITs, Utilities, MLPs, High Yield Bonds are a few examples. Reduce risk by dollar cost averaging.

2026. Manage the risks you can.

It’s WLA’s view that a decline in rates is low probability and low reward for traditional bond investors.If I am wrong, stocks probably outperform bonds…said another way, force lower rates –> hard assets might do well and maybe equities, too.

I don’t know if stocks will endure a broad based correction in 2026. If yes – WLA’s fixed income exposure is income producing, liquid cash equivalents and can be deployed to risk assets at lower entry points.

I don’t know what the price of oil is going to do. WLA is long energy equity and MLP exposure.The portfolio benefits from rising energy costs and receives attractive income from its energy exposure.

I don’t know how the Federal Government is going to manage its debt / spending / trade problem. WLA is long gold – a great hedge against poor policy.

I don’t know what inflation will do in 2026 (high or really high). WLA’s portfolio is cushioned with 2 out of 3 silos producing attractive income plus various inflation defensive positions. If rates blow out to 5%, WLA will reload the laddered bond portfolio.

WLA’s portfolio methodology:

Silo 1: Short-term treasuries currently with 3.5% - 4% yields.

Silo 2: US Equity. Endure the volatility, rebalance to lower entry points on weakness.

Silo 3: The satellite portfolio includes attractive total return positions, numerous fixed income alternatives paying 3 – 8% yields, positions with low correlation to Mag7, inflation defensives and various commodities.

Learn more about WLA’s portfolio:

https://westernlevel.com/commentary/october-2025-portfolio-update

Not investment advice. Performance figures are sourced from the following ETF links. Above performance figures are not representative of WLA client results, WLA client performance is based on different time periods among other factors. Actual client performance varies based on multiple factors including risk tolerance, when WLA was hired and when positions were established and the deduction of WLA ‘s management fees. WLA client holding period for the above examples varies, do not assume it’s the year to date period for any of the examples provided, it may be longer or shorter. Do not assume every WLA client holds every ETF example, client risk tolerance and when WLA was hired effects portfolio allocations. Read the disclosures on the ETF links provided. Performance listed is for illustration purposes only, not an endorsement to buy or sell. Do you own research and/or discuss with a professional investment advisor. Read full disclosures located in this email and at www.westernlevel.com.

ETF Links in the chart:

https://www.ssga.com/us/en/intermediary/etfs/state-street-spdr-sp-500-etf-trust-spy

https://advisors.vanguard.com/investments/products/bnd/vanguard-total-bond-market-etf?cmpgn=FAS:PS:XX:LF:20260311:GG:DM:LB~FAS_VN~GG_KC~BD_PR~High_UN~FIProductT1_MT~Exact_AT~None_EX~None:None:NONE:NONE:KW:BND&gclsrc=aw.ds,aw.ds&=null&gad_source=1&gad_campaignid=23601476609&gclid=Cj0KCQjw4PPNBhD8ARIsAMo-icwBuC-djTPccxs3L10VI2gFjjRqxCfZSMkOGVWSSz9JYqtmAoaXXvsaAgT6EALw_wcB

https://www.troweprice.com/financial-intermediary/us/en/investments/etfs/total-return-etf.html

https://www.ishares.com/us/products/331752/ishares-flexible-income-active-etf

https://www.pimco.com/us/en/investments/etf/pimco-investment-grade-corporate-bond-index-exchange-traded-fund/usetf-usd