DEC 2024: US Equity Flows

US Equity has had an outstanding 2024.

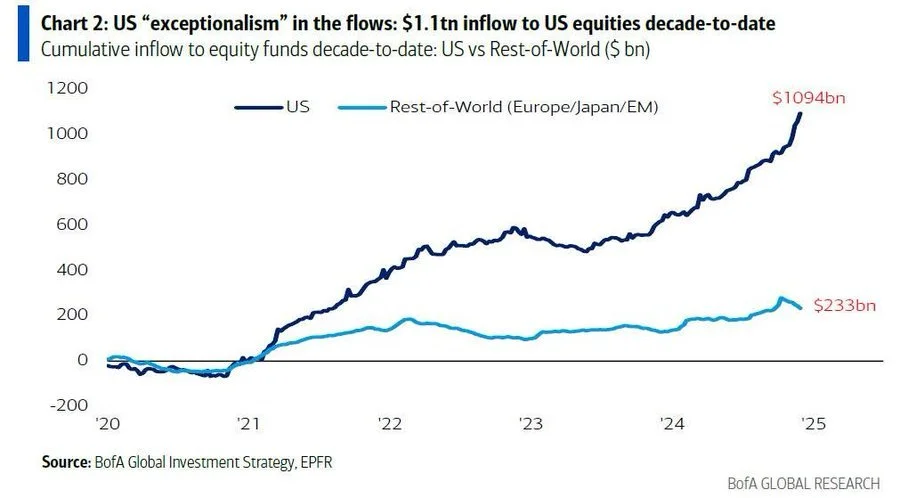

US Equity flows are record strong.

2025 Playbook.

When Non-US contra, if ever?

US Equity is the biggest beneficiary of investment flows in 2024 buy a wide margin. The capital flow trend has been steady for over ten years and the performance supports the trend. US Equity has trounced all broad International Equity and Emerging Market Equity indices in terms of performance for over ten years now.

Can the US Equity market strength continue?

Yes it can – earnings strength needs to continue. Given how high earnings expectations are, I expect volatility in 2025 and plan to boost exposure on any potential market weakness. In recent months I’ve been building positions in equal weighted US Equity ETFs and have also been adding to a US Large Cap Value tilt. I am also planning to add a US Equity Mid Cap position. These examples are intended to be more conservative relative to some of the high flying US Equity Growth categories where valuations are the richest.

2025 Playbook:

If US equity markets march higher – it’s US Exceptionalism.

If US Equity markets are derailed – it’s a buying opportunity.

When Non-US contra, if ever?

(When do we become contrarian – are international markets are too cheap?)

With International Equity under-performing the US Equity market for such a long and deep period (nearly 15 years) you would think this might be a contrarian entry point...and relative to how expensive certain sectors of the US Equity market have become, Non-US Equity is starting to gain my attention. If I’m going to allocate capital outside the US, I want low-correlated total return and high dividends are one appealing manner to achieve this objective. One fund I am reviewing has a dividend yield of just under 6%...so I am turning the corner. For equity exposure across the Non-US and Emerging Markets – I believe active management is the better path. That is – don’t expect “S&P 500 type exceptionalism” from a passive allocation to the MSCI EAFE. None-the-less, given the extreme US vs Non-US contrast (valuations, sentiment, performance, etc) it is worth watching closely and I’m officially considering exposure to Non-US Equity.

Two noteworthy articles about Non-US Investing:

https://www.ssga.com/us/en/intermediary/insights/how-long-can-the-us-market-outperform-the-world

https://www.morningstar.com/stocks/revisiting-case-international

The Charts:

Below is a simple 5 year chart of the S&P500 vs the EAFE and EAFE Emerging Markets indices (Non-US examples). This trend has been the case for over 10 years...see the links above for more detailed analysis.

Let’s agree that the EU doesn’t do Technology…another reason not to be a passive investor outside the US.

Have a great holiday season…let’s get some snow on the mountain!

Best,

Jon Fritzinger

Founder / CEO

Western Level Advisors LLC

Hello@westernlevel.com

About Western Level:

Western Level Advisors LLC is an independent Registered Investment Advisor. The firm provides investment management and long-term financial planning services for individuals. All services are provided on a fiduciary and fee-only basis. Western Level’s only purpose is to establish a clear pathway for each client to help them manage and compound their wealth.

The information provided in this commentary is intended to be informative and not intended to be advice relative to any investment or portfolio offered through WLA. The views expressed in this commentary reflect the opinion of the author based on data available as of the date this commentary was written and is subject to change without notice. This commentary is not a complete analysis of any sector, industry or security. This commentary is not intended to be a recommendation to buy or sell any investment. Please contact WLA with any questions regarding your accounts. The information provided in this commentary is not a solicitation for the investment management or other services offered by WLA. References incorporated into the commentary from third party sources are as of the date specified and are believed to be reliable. WLA is not responsible for errors in the third party data. Source information is provided under each chart. Additional disclosures are available at www.westernlevel.com.